It's really all symantics. If you have two twins each take out a 100,000 UL policy and one guy pays a month premium and the other puts in $50,000 and both die at the same time in a car accident a few days later, both beneficiaries are receiving $100,000 and the $50,000 is gone. Net amount of risk or not the company is keeping that $50,000 if the UL is option A.

The $50,000 is paid out as a part of the total $100,000 death benefit proceeds. The twin who paid $50,000 would've simply had a lower cost of insurance because the amount at risk was only $50,000. If the insurance company "kept the cash values", then they would only be paying out the amount at risk, which, in this example would be $50,000.

While the other twin who only made 1 monthly payment is paying for the entire $100,000 which is the amount at risk.

But yes, both beneficiaries would still receive the $100,000 death benefit check.

The $50,000 is paid out as a part of the total $100,000 death benefit proceeds. The twin who paid $50,000 would've simply had a lower cost of insurance because the amount at risk was only $50,000. If the insurance company "kept the cash values", then they would only be paying out the amount at risk, which, in this example would be $50,000.

While the other twin who only made 1 monthly payment is paying for the entire $100,000 which is the amount at risk.

But yes, both beneficiaries would still receive the $100,000 death benefit check.

Once again it's really just symantics. But one family is out $50,000 because the company kept it. If the companies pay a death claim based on the net amount of risk formula you would think they would of changed the annual report to show it. The annual report as you know shows the death benefit and the cash surrender value only.

They both bought a $100,000 death benefit, the one family is out because the insurance company keeps the cash value. It's really that simple.

The net amount of risk in a UL is the difference between the death benefit and the cash value. That number is then multiplied by the rate per thousand and deducted monthly for the insurance cost. It has nothing to do with the death benefit payable that is why it is not on the annual statement in the death benefit calculation.

Yes, I'm arguing semantics, because life insurance is a contract and contracts are defined by various terms, and each term has a specific definition.

If the insurance company paid out the "face amount", then the insurance company "keeps the cash value". Of course, the "face amount" is just the beginning of the calculations of a life insurance policy illustration.

The death benefit column is called... total death benefit, NOT "face amount".

The death benefit and face amounts are two different numbers used in different context.

Therefore, the death benefit is defined as:

Net death benefit = cash values + amount at risk - any outstanding loans.

If you can find me an illustration that shows a column for 'face amount'... then you will be correct because then the insurance company will be paying out the 'face amount' regardless of cash values... that they would (supposedly) keep.

It shows the base death benefit and in a whole life policy any paid up additions minus policy loans. And that's the death benefit. The cash value on the statement is not payable unless its an option B UL.

In today's litigious society if they calculated the death benefit like you, your DB calculation would be on the annual report. It's because the death benefit is made up of the face amount listed in the policy, PUA's and loans. Net amount of risk is not part of the equation.

Okay, I've attached HS311 regarding net amount at risk. I'm sure it's been a while since you took your CLU and ChFC courses, but this is in the current textbook available via the Professional Resource Center at The American College.

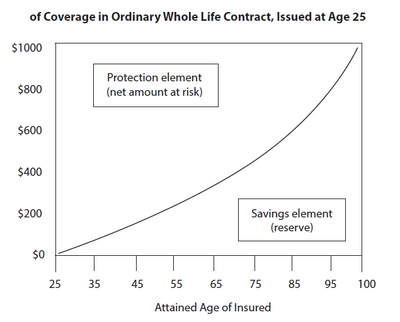

Under a cash value contract, the accumulated reserve becomes part of the face amount payable at the insured’s death. From the standpoint of the insurance company, the effective amount of insurance is the difference between the face amount of the policy and the reserve. This amount is called the net amount at risk. As the reserve increases, the net amount at risk decreases if the face amount remains constant.

A cash value life insurance policy does not provide pure insurance but a combination of protection and cash values, the sum of which is always equal to the face amount of the policy.

The area below the curve represents the reserve under the contract or, as mentioned above, the policyowner’s equity in the contract. The area above the curve represents the company’s net amount at risk and the policyowner’s amount of protection. As the reserve increases, the amount of pure protection decreases. At any given age, the two combined will equal the face amount of the policy.

I do remember that chart and after looking at it again it has made me realize whole life is a TERRIBLE insurance plan your younger people.

1. You start out paying 3 or 4 times the cost of term.

2. As the years go by the net risk amount of risk to the insurance company is going down but your still paying the same premium.

3. If you die you only get the death benefit ,whereas with a 30 term and a Roth both the death benefit and the IRA are paid out tax free.

4. The money is not yours in a whole life you need to borrow it whereas a Roth it's yours and no need to pay intrest.

5. The 3 or 4 percent a whole life may make over a 30 period is overstated because once you withdraw that money you will be paying interest on it every year. OUCH!! A Roth is tax free and intrest free.

6. If you still need insurance after 30 buy a little policy because really that's all you would have if you started out with whole life because of the net amount of risk.

As I stated before I'm not a termite and sell a lot of permanent life insurance but mainly for wealth transfer.

")

")