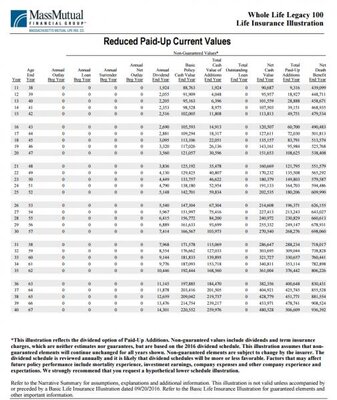

TheLifeGuy

New Member

- 9

Would appreciate some insight from those of you with familiarity with this contract.

Will they allow their clients to use the PUA rider with flexibility from year to year to fund the policy? IE can you pay it one year and not pay it again for 7 years and then pay it for 5 in a row. Mass does not. After 1 year of missing payment you must pay it or it comes off permanently.

What is their allowable premium to pua ratio? I know Mass will not allow more than 9X's the premium to be added to the ALIR rider.

Any clarity on the Chronic Illness Rider and differences between the LTC rider on the Mass contract? Mass will not allow you to RPU a contract and receive the benefits of the LTC rider. Also, the LTC monthly benefit is based on the premium portion of the total initial premium, so if you want a blended whole life contract with max cash your LTC monthly benefit is poor. These 2 things leave you with a basic 10 pay policy. My understanding is Penn's rider is based on the death benefit at time of claim.

Finally, our GA suggested that Mass's dividend could take a big fall this year and thus making the Penn blended whole life contract even more attractive.

Thoughts? Thank you in advance.

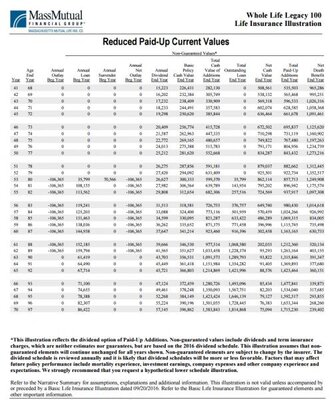

Will they allow their clients to use the PUA rider with flexibility from year to year to fund the policy? IE can you pay it one year and not pay it again for 7 years and then pay it for 5 in a row. Mass does not. After 1 year of missing payment you must pay it or it comes off permanently.

What is their allowable premium to pua ratio? I know Mass will not allow more than 9X's the premium to be added to the ALIR rider.

Any clarity on the Chronic Illness Rider and differences between the LTC rider on the Mass contract? Mass will not allow you to RPU a contract and receive the benefits of the LTC rider. Also, the LTC monthly benefit is based on the premium portion of the total initial premium, so if you want a blended whole life contract with max cash your LTC monthly benefit is poor. These 2 things leave you with a basic 10 pay policy. My understanding is Penn's rider is based on the death benefit at time of claim.

Finally, our GA suggested that Mass's dividend could take a big fall this year and thus making the Penn blended whole life contract even more attractive.

Thoughts? Thank you in advance.