I've read several posts started by others and greatly appreciate the time other people have put into educating us consumers. My situation is similar to threads started by mx_599, johnyblu, slick_spe3, and luxlux. Quick background:

- Married healthy male 31, one child, a second on the way (might qualify for the highest tier, definitely should qualify for the preferred tier, using term4sale's mini calculator).

- Have an emergency fund, and am maxing out 401k and Roth IRA.

- Plan to keep this new policy long term.

- Cash value accumulation is of primary importance, death benefit is an important but secondary benefit.

- Would like to "front fund" the policy as much as possible without triggering MEC.

- In 10 years or so, I would like the flexibility to stop paying all premiums (primary concern). If possible, would like the option to continue funding to grow the cash value as well.

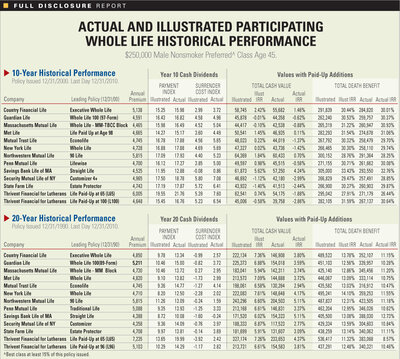

- Basically, will treat the WL policy as a conservative part of my after tax investment portfolio, so cash value accumulation (and associated IRR) is the most important factor for me.

From what I've read, a 10 pay WL policy with a term rider and the maximum amount of paid up additions is the route I should go. Does anyone have any other suggestions for my situation?

Specific questions:

1) What happens at the end of a 10 pay WL policy? Am I able to continue to add to the policy? How do I make sure I don't put too much into it and make it a MEC?

2) How important is a disability rider? Would it be less expensive to get a separate disability policy?

3) I haven't been able to find much on the variance in the IRR from different companies. Shouldn't I focus on companies that have historically had a higher IRR?

Thanks for your help!

- Married healthy male 31, one child, a second on the way (might qualify for the highest tier, definitely should qualify for the preferred tier, using term4sale's mini calculator).

- Have an emergency fund, and am maxing out 401k and Roth IRA.

- Plan to keep this new policy long term.

- Cash value accumulation is of primary importance, death benefit is an important but secondary benefit.

- Would like to "front fund" the policy as much as possible without triggering MEC.

- In 10 years or so, I would like the flexibility to stop paying all premiums (primary concern). If possible, would like the option to continue funding to grow the cash value as well.

- Basically, will treat the WL policy as a conservative part of my after tax investment portfolio, so cash value accumulation (and associated IRR) is the most important factor for me.

From what I've read, a 10 pay WL policy with a term rider and the maximum amount of paid up additions is the route I should go. Does anyone have any other suggestions for my situation?

Specific questions:

1) What happens at the end of a 10 pay WL policy? Am I able to continue to add to the policy? How do I make sure I don't put too much into it and make it a MEC?

2) How important is a disability rider? Would it be less expensive to get a separate disability policy?

3) I haven't been able to find much on the variance in the IRR from different companies. Shouldn't I focus on companies that have historically had a higher IRR?

Thanks for your help!

Last edited: